Payroll And Taxes

With the population of 1.2billion people, India is the seventh largest country in

the

world with an average growth rate of 5.8% per year. Recently India has achieved

remarkable growth in pharmaceuticals, petroleum, software and biotechnology

industries.

India’s huge population and economic growth also make the country a very attractive

market for foreign investors and products. In the year 2011, it was ranked as the

10th

largest importer and the 19th largest exporter in the world.

The rapid growth in industrialization gives a high rise in employment rate and

different

kind of taxes. Understanding of these taxes is very important for every employee and

employer to avoid any complications. This article will give you a clear idea about

the

calculation of payroll and taxes in India.

Payroll Options in India

There are plenty of options available regarding the development and application of

payroll system.

-

Fully Outsourced Payroll Department

Foreign companies who are operating or want to extend their business boundary to India, could face a lot of difficulties in understanding and comply with tax rules applicable in India. To avoid all these difficulties, foreign companies can outsource their payroll to third party companies, who will pay on their behalf.

-

Internal Payroll

Foreign or local companies, which are registered in any available business form, and make their own internal payroll system will have to follow the local laws at the time of salary disbursement.

Calculation of Payroll

Payroll is generally the list of employees, employed in any business or non-business

entity. Payroll also refers to the total amount of money the employer pays to the

employee against the services provided.

The pay slip of the employee should consist of all the benefits allowed to the

employee

like basic pay, variable pay, and allowances. The employer is liable to deduct all

the

necessary taxes and other deductions according to the law and regulations. So the

net

pay would be termed in mathematical form as

Net pay = Gross Pay – All necessary deductions

While,

Gross pay = All type of basic pay + allowances + any other special benefit

Necessary Deductions= All basic type deduction – deductions applicable under law

+ any other special deduction.

Deductions from payroll are normally TDS, PF, ESI, and PT, etc.

- TDS can be calculated as (Basic salary + allowance – deductions) *12 – IT deductions

- PF or Provident fund is 12% of the basic salary of 15% whichever is lower

- While ESI amounted to 1.75% of 21000 or gross pay, whichever is lower.

Salary structure for 2018-2019 with all the tax details are as follows:

| Element | Taxation Treatment | PF applicable | Part of Gratuity | Minimum Amount |

| Basic Salary | Fully taxable | Yes | Yes | As per Minimum wage |

| DA | Fully taxable | Yes | Yes | As per Minimum wage |

| Medical & Convenience | Fully taxable | No | No | None |

| HRA | Exempt up to the following 3 conditions 1.Actual HRA 2.50% of basic salary+40% of Basic if DA is metro+ DA if non metro 3. 10% of basic rent |

No | No | Depends on the state |

| LTA | Actual expense | No | No | None |

| Education Allowance | For 2 children Rs.100 | No | No | None |

| Car Maintenance | 2400 per month | No | No | None |

| Driver Salary | Driver salary up to 900 | No | No | None |

| Special Allowance | Fully Taxable | No | No | None |

Details of Deductions and their calculation:

| Name of Deductions | Calculation | Application |

| PF (Provident Fund) | 12% of basic salary + DA + Any special allowance | Companies with 20 or more employees. Apply on all the employees whose basic + DA + Special is less than 15,000 INR per month. |

| ESIC | Employer contribution = 4.75% Employee contribution = 1.75% |

Companies with 20 or more employees, whose salary per month is less than 21,000. |

| Professional Tax | Every state have their own rules | All employees where this is applicable |

| labor Welfare Fund | Every state have their own rules | All employees where this is applicable |

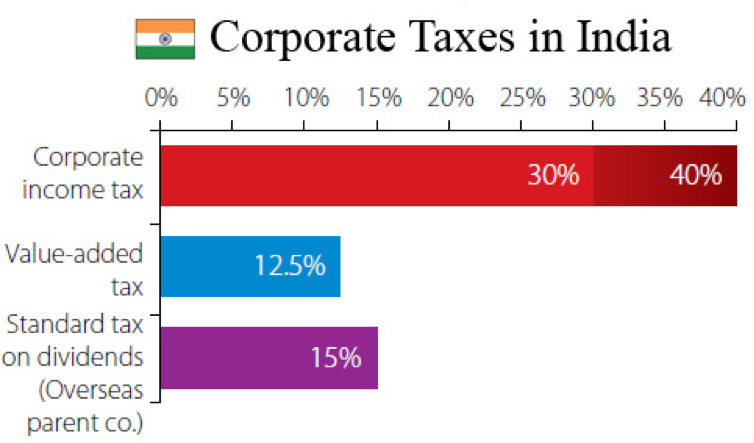

In addition to all these taxes, there are another type of tax known as income tax is also applicable on the individuals who’s income falls in that category is called income tax.